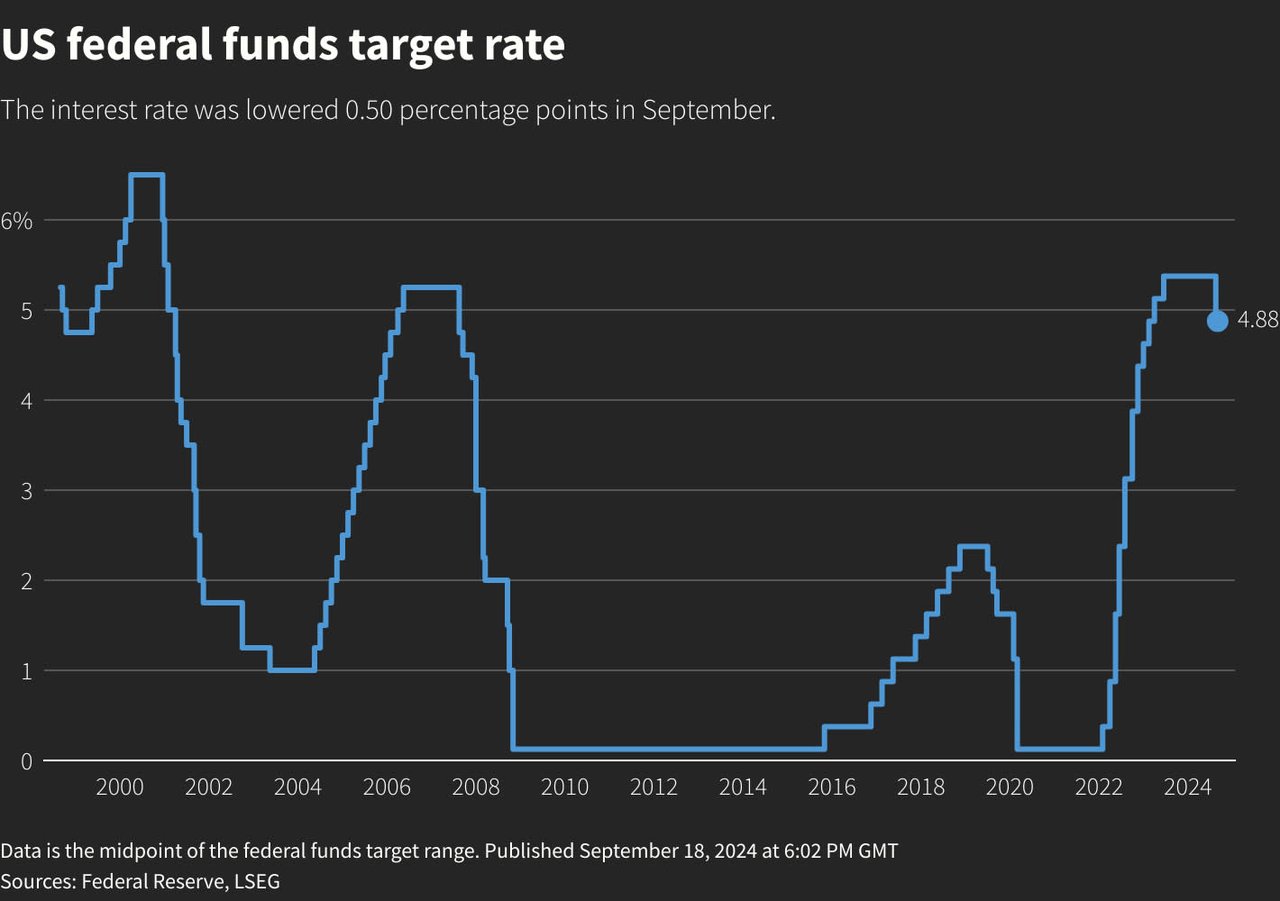

Big news—yesterday, the Fed announced the first rate cut in four years, dropping the federal funds rate by 0.5%. This is a significant shift after years of rate hikes meant to control inflation, and it signals a change in direction. But let’s be clear: this doesn’t mean your mortgage rate is going to drop by 0.5% overnight. It’s not that simple.

Why Did the Fed Cut Rates?

For the last few years, the Fed has been raising rates aggressively to battle inflation, which was out of control—peaking at 9.1% last year. Fast forward to today: inflation is down to 2.5%, which is pretty close to the Fed’s target. But here’s the kicker: the economy is starting to slow down in other areas, like the job market. The Fed knows it needs to act before things start to grind to a halt, so they cut rates to keep things moving.

The Truth About Mortgage Rates

Now, I know what you’re thinking: if the Fed just cut rates, why didn’t mortgage rates drop by the same amount? That’s a common misunderstanding, and it’s important to remember that mortgage rates don’t follow the Fed rate directly. They’re influenced by things like the 10-year Treasury yield, inflation, and overall economic conditions.

As Wendy Rogers from Edge Home Finance said: "Mortgage rate markets were expecting this rate cut, so there was no real change yesterday. But mortgage rates are already trending downward, and we're seeing some of the lowest rates we’ve had in two years. More cuts are expected in the coming months, so it’s a step in the right direction for buyers and homeowners."

Translation: even though there wasn’t a huge drop yesterday, mortgage rates are still low. If you’re in the market to buy or refinance, you’ve got some opportunities right now.

How a Rate Cut Affects Different Mortgage Types

The impact of the Fed’s rate cut varies depending on the type of mortgage you have or are considering. Nellie Dallman, Chief Operating Officer at Results Home Mortgage, breaks it down:

-

Adjustable-Rate Mortgages (ARMs): "ARMs are more closely tied to the prime rate and short-term interest rates. With this Fed rate cut, consumers with existing ARMs could see their payments decrease, and new borrowers could secure more favorable rates."

-

Fixed-Rate Mortgages (FRMs): "Fixed-rate mortgages are influenced more by long-term interest rates, like the 10-year Treasury yield. While the Fed’s rate cut doesn’t directly lower fixed mortgage rates, it can influence long-term bond yields, which may eventually bring down fixed-rate mortgage rates. But inflation expectations and broader economic conditions also play a role."

What’s Happening with Mortgage Rates Right Now?

The 10-year Treasury yield—which is a key driver for mortgage rates—had a bit of movement following the Fed’s announcement. It dipped briefly but bounced back up later in the day. When the 10-year Treasury yield goes up, mortgage rates tend to worsen; when it goes down, mortgage rates improve.

Scott Roiger, Senior Loan Officer at Bay Equity, offered some insight: "It’s tough when news like this comes out because everyone thinks mortgage rates should immediately drop by 0.5%. But that’s not how it works. A lot of the rate movement was already priced in, and we even saw a slight worsening of rates in the morning before the announcement. As time goes on, though, we might see some additional decreases in mortgage rates."

Opportunities for Homebuyers and Homeowners

The Fed’s rate cut could bring opportunities for both buyers and homeowners:

-

For Buyers: Mortgage rates are low, so if you’ve been on the fence, this is your moment. Lower rates mean you can afford more home for your money, which could bring more homes into your budget.

-

For Homeowners: If you’re thinking about refinancing, now might be the time to act. Even though rates didn’t drop drastically yesterday, locking in now could still save you money or shorten your loan term. Nellie Dallman adds, "Homeowners with existing ARMs may benefit from a rate reset at a lower level, leading to reduced payments."

Increased Competition

Lower mortgage rates can encourage more buyers to enter the market, potentially driving up demand. Nellie Dallman warns, "With lower mortgage rates, we could see more competition, which might increase home prices in competitive markets. Consumers should be prepared for potentially higher bidding wars if demand outpaces supply."

Looking Ahead

Another Fed meeting is coming up on November 7, and they could cut rates again. If that happens, we might see even lower mortgage rates heading into 2024 and 2025. But like I always say, don’t wait around for something that isn’t guaranteed. The market is giving you an opportunity now—take advantage of it while you can.

Bottom Line

This rate cut shows that the Fed is focused on keeping the economy steady while inflation remains under control. It’s a signal for buyers and homeowners to seize the moment with low mortgage rates that are already in place. With another potential rate cut on the horizon, there’s a lot to be optimistic about—but timing is everything.

If you’re ready to talk strategy or want to know how this impacts your specific situation, let’s connect. Whether you’re buying, refinancing, or just curious, I’m here to help guide you through it.

Contact Information for Expert Quotes:

Wendy Rogers

Mortgage Loan Originator

Edge Home Finance

C: (612)-247-0924

4510 W 77th St Ste 380, Edina, MN 55435

[email protected]

Scott Roiger

Senior Loan Officer

Bay Equity Home Loans

P: (507) 226-2288

10591 165th Street West, Lakeville, MN 55044

[email protected]

Nellie Dallman

Chief Operating Officer

Results Home Mortgage

Direct/Mobile: (763) 218-2487

11200 W 78th Street, Suite 50, Eden Prairie, MN 55344

[email protected]